Most risk-averse masses stay away from investing due to the “fear” of losing money and missing out on the right market timing. Contrary to the lump sum strategies, Dollar cost averaging is one of the conservative approaches that can possibly cater to the dynamics of such apprehensive investors. The DCA strategy mitigates the effects of market volatility and minimizes overall risks by spreading out asset purchases.

Let us look in more detail at what is dollar-cost averaging and how it can help investors multiply their wealth over time.

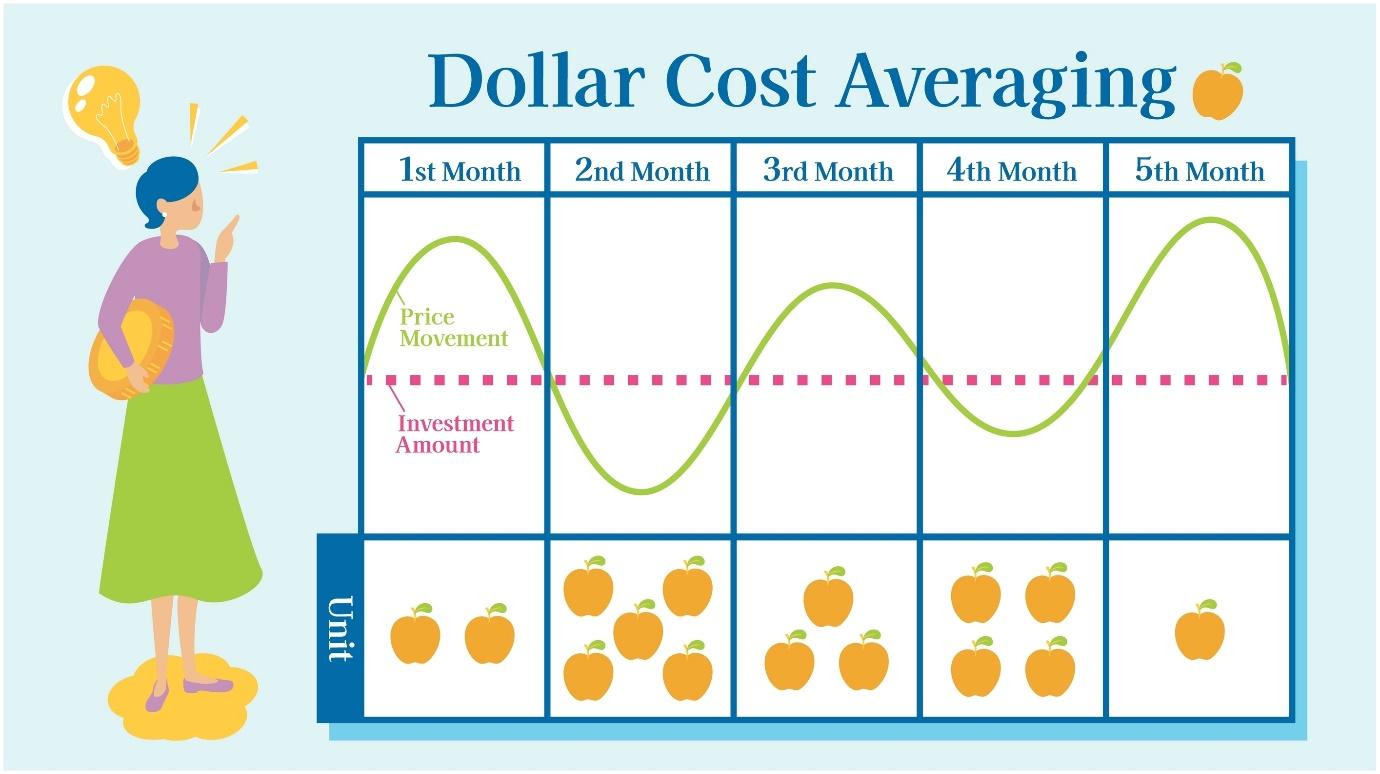

What is dollar cost averaging?

Dollar-cost averaging is an investing strategy that involves dedicating equal portions of an allotted amount to be used for purchasing a particular stock/mutual fund/ some other asset over time in periodic cycles. The main purpose of this technique is to save investors from the hassle of constantly predicting market movements and pinning down a specific best time to buy a security.

As it might be apparent from the strategy’s name, it is based on the “average” concept – where you keep investing fixed amounts at regular intervals even if the price is low, high, or stagnant. Consequently, the overall outcome is smoothened or averaged out.

Most professionals term the dollar-cost averaging methodology to be ideal for long-term investment growth due to its consistent and relatively secure nature.

How does dollar cost averaging work?

To start with the dollar cost averaging strategy, it is important to first decide on your total investment amount, how much you want to input per interval, and whether you’ll make contributions weekly, bi-weekly, or monthly.

After determining your plan, you can set up a brokerage account and automate your investments for a more convenient and efficient experience.

Now, to better understand how DCA works, let us look at an example.

Suppose you plan to invest a total of $1500 in an XYZ company. With dollar cost averaging, you decide to infuse $150 per month for buying the XYZ shares. It means you might be able to purchase more shares in some months while less in other months because your monthly contributions are ‘pre-determined’ regardless of the present market direction.

Here’s a hypothetical illustration of how $1500 would be divided to buy stocks over the span of 10 months.

| Month | Monthly Contribution | XYZ Share Price | Shares Purchased |

| January | $150 | $15 | 10 |

| February | $150 | $12 | 12.5 |

| March | $150 | $15 | 10 |

| April | $150 | $13 | 11.5 |

| May | $150 | $12 | 12.5 |

| June | $150 | $14 | 10.7 |

| July | $150 | $10 | 15 |

| August | $150 | $12 | 12.5 |

| September | $150 | $9 | 16.6 |

| October | $150 | $10 | 15 |

As per this example, you will own a total of 126.3 shares by the end of 10 months if you keep investing $150/month.

Dollar-cost averaging vs lump sum investing: Comparing results

While you can make intermittent investments via dollar cost averaging, there is always an option to invest the whole “lump sum” collectively at one time.

Here’s how lump sum investment will compare to the DCA if we apply it to the above-mentioned example.

| Month | Invested Amount | XYZ Share price | Shares Purchased |

| January | $1500 | $15 | 100 |

| February | $0 | $12 | 0 |

| March | $0 | $15 | 0 |

| April | $0 | $13 | 0 |

| May | $0 | $12 | 0 |

| June | $0 | $14 | 0 |

| July | $0 | $10 | 0 |

| August | $0 | $12 | 0 |

| September | $0 | $9 | 0 |

| October | $0 | $10 | 0 |

As can be seen on the chart, you invested all $1500 at once and buys 100 shares of XYZ company.

According to this illustration, you will end up with more shares using the DCA technique (126.3 shares) than if you had bought all shares altogether at the start (100 shares). So, when the XYZ stock surges in value over the long term, you would end up earning more profits with the DCA strategy.

However, that is not to say that lump sum investing cannot outperform dollar cost averaging. In many real-world cases, you might be better off investing the whole sum collectively, especially if it’s a large amount as DCA does not always work out perfectly.

Pros of dollar cost averaging

Dollar-cost averaging holds its reputation due to a number of key advantages, which are as follows:

- DCA lowers the entry barriers for investors, meaning you can start investing with small amounts of money without waiting to gather a large sum for entering the markets. Consequently, this technique offers optimal investing opportunities to young investors who do not own much-accumulated wealth. Moreover, the low-cost entry is also beneficial for risk-averse individuals who do not wish to invest all their money at once.

- Dollar-cost averaging is a systemic investing procedure that allows you to gradually build up your wealth over time.

- DCA ensures regular investments during falling markets which mostly translates into remarkable future growth. While investing during a time when all investors are dumping their assets is pretty terrifying, history shows that markets move in cycles and bearish prices eventually rebound to extend tremendous returns on investments. Moreover, Charles Schwab research shows that those who remain invested or keep investing in crashing markets witness better results than those who try to time the market.

- Dollar-cost averaging takes out the emotional element from investing. Psychological ups and down can adversely affect the trading results and DCA is a reliable way to take out emotions from investing.

Cons of dollar cost averaging

Here are some points you should keep in mind before choosing the DCA approach.

- You might have to pay more transaction fees due to repeatedly investing at regular intervals.

- If you have a large sum of money, sitting on your cash (as in the case of DCA) might not be a good option as you can miss out on potential gains.

- DCA is not suitable for dividend-paying stocks.

- DCA is not a zero-risk strategy. As mentioned before, there may be times when you buy stocks at expensive prices.

Is dollar cost averaging a suitable strategy for you?

While dollar cost averaging has a competitive advantage most of the time, it might not be beneficial in all cases. Its suitability varies from person to person as per their preferences, risk tolerance, and the amount they’d like to invest. Moreover, there is also an element of “luck”, or “research” you could say, where the investors who ideally “buy the market dip” would be more profitable than DCA investors.

Nonetheless, dollar cost averaging may be right for you, if:

- You are a beginner investor with no large amount at hand.

- You want to avoid extensive market research and tracking the market at all times.

- You want to invest with a relatively safe and calculated approach.

- You are in no hurry to acquire explosive gains in a short period.

Read more:

https://thetradingbay.com/everything-you-need-to-know-about-futures-trading/

https://thetradingbay.com/understanding-arbitrage-what-is-arbitrage-how-does-it-work/